This audio is automatically generated. Please let us know if you have any comments.

Dive brief:

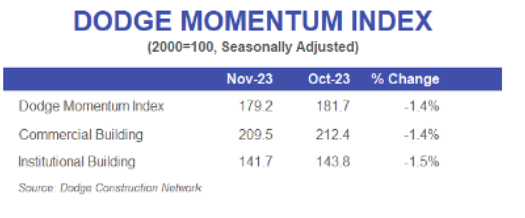

- The Dodge Momentum index, a benchmark that measures nonresidential building planning, fell 1.4% in November, mainly due to a slowdown in business planning, according to the Dodge Construction Network. During the month, both the commercial and institutional components fell around 1%.

- The fall in November compensated Increase of 1% in Octoberwhere slight growth in warehouse activity helped push the index back into positive territory for the first time in six months.

- “While both parts of the Momentum index experienced a slower pace in planning, overall levels remain stable and will support construction spending in 2024 and 2025,” said Sarah Martin, associate director of Dodge Construction Network forecast. “Non-residential planning activity will remain constrained by stronger growth amid current labor and construction cost challenges.”

Diving knowledge:

High interest rates, supply chain disruptions and tighter lending standards continue weigh in the commercial segmentthat includes office, retail and warehouse projects, Martin said.

Excluding data center activity, all published business segments decrease in planning levels in November, according to Dodge. This negative trend has dominated much of 2023, as planning activity in the commercial segment now remains below levels of about 20% ago.

At the institutional level, the persistent weakness in educational planning continues to offset the positive momentum in health and public projects. Despite that friction, the institutional segment is still up 2% from a year ago, largely due to the sector’s resilience so far to market headwinds, Martin said.

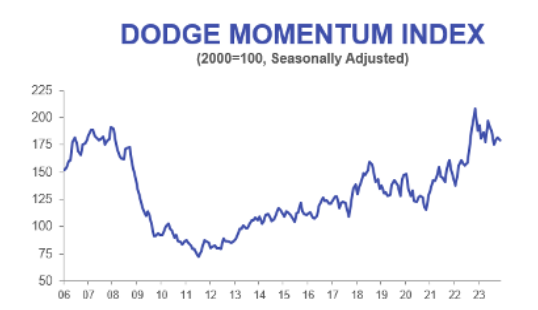

Year over year, the global DMI was 14% lower than in November 2022.

“Business planning has generally been in decline since its peak last year, but has begun to stabilize in recent months,” Martin said. “By comparison, from an institutional standpoint, we’re only seeing slightly more positive momentum trends through 2023.”

Architectural turnover continues to fall

Meanwhile, the Architectural Turnover Index, which also provides a leading indicator for upcoming construction jobs that are nine to 12 months away, continues to plummet, according to the most recent data from the American Institute of Architects. The ABI score fell to 44.3 as more companies reported a decline in business turnover than the previous month. Any mark below 50 indicates a contraction in activity.

Indicators of future work in the pipeline also stumbled, as firms reported a fall in new project inquiries for the first time since July 2020, according to the ABI report. In addition, the value of newly signed design contracts also softened for the third month in a row, the report said.

“Things seem to have slowed down since the summer, and we are working on backlog projects. Fewer projects and calls are coming in, and new projects seem to be fewer and smaller,” according to a trading company cited in the report of the AIA. “We expect it to be a year-end slowdown, but we’re preparing for a slower 2024.”

A total of 17 projects valued at $100 or more entered the planning stages in November, according to Dodge. Major commercial projects include:

- The $480 million Project Cosmo Data Center in Cheyenne, Wyoming.

- The $300 million Sherwin Williams headquarters building in Cleveland, Ohio.

The largest institutional projects to enter planning included:

- The $315 million second phase of FSU Health Hospital in Tallahassee, Florida.

- The $258 million LA Convention Center showroom in Los Angeles.