Election jitters are affecting construction activity, although public sector projects continue to move forward, at least for now.

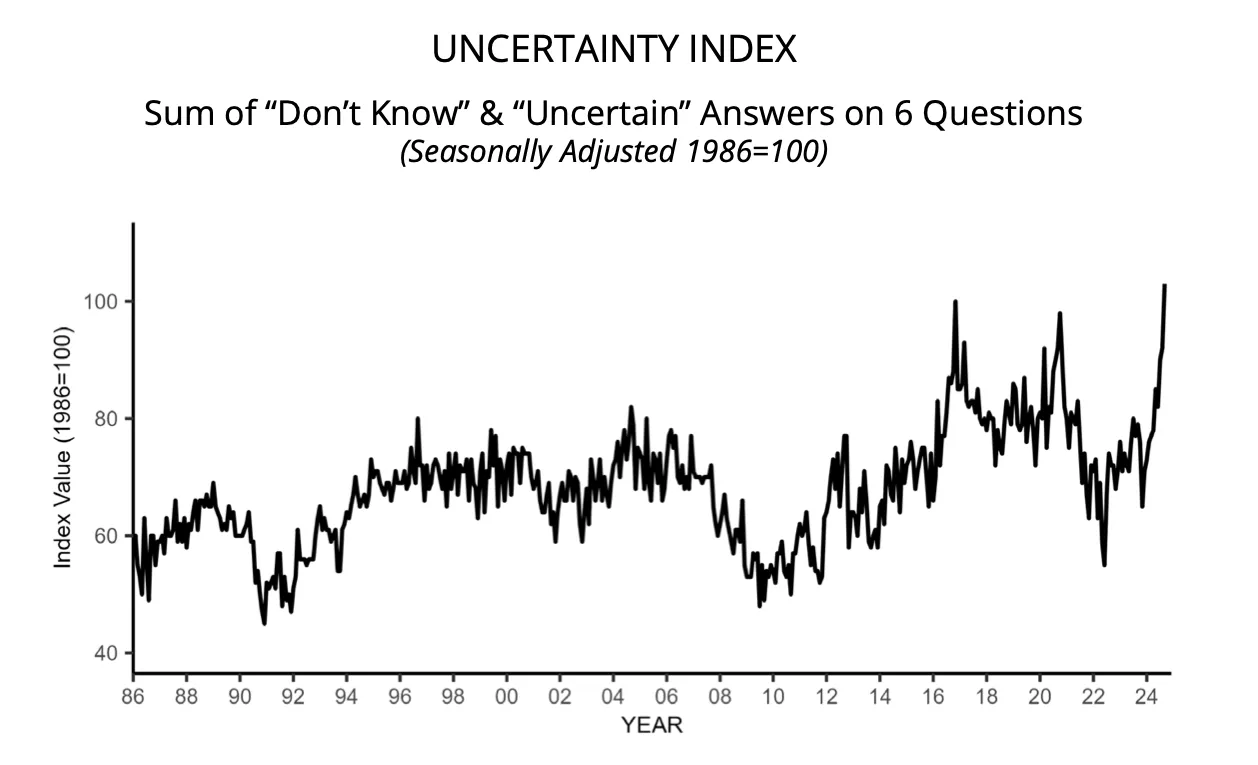

Uncertainty has recently reached small business owners in all industries a historic highaccording to the latest index from the National Federation of Independent Business, a trade group representing smaller businesses. That anxiety, which comes during one of the tightest presidential contests in recent memory, is affecting overall construction activity, industry professionals told Construction Dive.

Courtesy of the National Federation of Independent Business

“We’re seeing uncertainty in the market about the potential economic impacts of the election,” said Granger Hassmann, vice president of preconstruction and estimating at Adolfson & Peterson, a Minneapolis-based construction management firm. “The overall market seems to have slowed down, especially in the private sector.”

And while the degree of uncertainty has increased in recent months, Hassmann added that the trend has become apparent over the past two years, with the slowdown exacerbated by a “let’s see what happens,” he said.

Farmer Hassmann

Courtesy of Adolfson & Peterson

Meanwhile, in the Fed’s latest Beige Book report, which provides commentary on current economic conditions, the Federal Reserve Bank of Cleveland noted that two unnamed commercial builders recently reported that many companies plan to wait until after the general election to undertake construction projects. New York construction firms also reported that activity there has slowed at a moderate pace, according to the Federal Reserve Bank of New York.

Omens of construction

Architecture firms, often early indicators of future construction activity, have also seen a slowdown. Design firms have felt that pinch as upcoming election clouds anticipated economic recovery, said Kermit Baker, chief economist at the American Institute of Architects.

“We had hoped that with the easing of inflation concerns and lower interest rates, there would be a recovery, but the election uncertainty appears to be inhibiting any expected recovery at this time,” Baker said. “[Architecture] Businesses pointed to the upcoming election as one of the main reasons for the expected weakness in the second half of the year.”

Kermit Baker

Authorization granted by the AIA

This hesitation can also be seen in other areas.

For example, electric vehicle battery manufacturer Ultium Cells recently shut down its $2.6 billion factory in Lansing, Michigan, due to sluggish demand and high interest rates. The company plans to resume the project once it has a clearer economic outlook, reflecting the broader wait-and-see strategy referred to by Hassmann.

And in Philadelphia, real estate developer Shift Capital has paused the conversion work in August at the historic Beury Building due to lender funding problems, CEO Brian Murray noted that high interest rates and lender caution have made banks wary of committing to large projects. This hesitation reflects more general concerns about the economic environment, including high interest rates and regulatory uncertainties.

That lack of clarity is fueling this cautious approach, as several potential outcomes could create different policy environments, said Michael Guckes, chief economist at ConstructConnect, a Cincinnati-based construction data provider.

Real estate developer Shift Capital halted work in August on the Beury Building in Philadelphia because of lender financing issues.

Courtesy of Shift Capital

“This issue, in general, is complicated because a lot depends on who controls not only the White House, but also Congress,” Guckes said. “There are many ‘divided government’ scenarios that would see the presidential plans of either candidate generally thwarted by an opposing Congress.”

Public projects are doing better

An exception seems to be infrastructure projects and public sector works.

Most public construction projects have a long lead time and create structures that are intended to be used for many years, so many property owners likely wouldn’t stick around after getting designs, approvals and financing, Ken Simonson said. , chief economist for the Associated General Contractors of America. AGC member companies have not reported election uncertainty as a reason for owners to stay in public jobs, he said.

Ken Simonson

Courtesy of AGC

“I think that public projects, [such as] infrastructure, schools, public safety, judicial structures, penitentiaries, data centers, utility projects and many manufacturing plants are particularly immune to election uncertainty,” Simonson said. “These are the categories with the best prospects for 2025” .

However, some funding packages, such as massive subsidies to manufacturers willing to invest in new domestic production capacity and alternative energy producers included in the CHIPS Act and the Inflation Reduction Act, could be substantially modified by a change of administration, said Anirban Basu, chief economist. to Builders and Associated Contractors.

“This seems especially true in the energy sector,” Basu said. “In one possible scenario, subsidies to alternative energy producers would be reduced, while support for more traditional forms of energy would be increased.”

For example, solar cell maker Meyer Burger recently dropped out $400 million plant project in Colorado due to financial constraints linked to the Inflation Reduction Act and an uncertain economic environment. This reduced their potential debt financing and consequently their construction funds.

Anirban Basu

Permission granted by ABC

Basu also pointed to broader economic trends affecting contractors.

For example, although the cost of construction materials is 39% higher than at the start of the COVID-19 pandemic, prices have remained more stable over the past two years. Recent falls in energy prices have helped maintain that trend, but Basu warned that a possible renewal of the trade war, especially with tariffs in China, would likely lead to higher construction costs.

He added that trade-related inflationary pressures could put upward pressure on interest rates, something contractors have longed to see calm.

A return to high rates?

If one party gains full control of the White House and Congress, the impact on construction would be more substantial, Guckes said.

A Trump presidency with a Republican sweep of Congress could lead to increased deficit spending, lower corporate taxes and higher tariffs. That would create a mixed growth environment in the near term with a possible second wave of inflation, Guckes said.

Assuming the Federal Reserve returns to its anti-inflation strategy in 2022 and 2023, higher interest rates would be used again to curb that inflation. Those hikes would deeply affect the ability of homeowners and developers to refinance new construction, Guckes said.

Michael Gucks

Courtesy of ConstructConnect

“A repeat of the 2022 rate hikes in 2026 or 2027 would negatively impact construction in the following year or years, as was the case in 2023 and 2024,” Guckes said. “ConstructConnect’s current expectation of 4% annual construction growth in both 2027 and 2028 would be at risk of significant downward revisions.”

Stricter regulations?

By contrast, a Harris administration with Democratic control of Congress would likely avoid aggressive spending in the near term, but could impose stricter environmental and labor regulations. That could also slow construction activity, Guckes said.

“Let’s wait for one [Harris administration to have a] less aggressive approach to drive short-term growth. This would allow the country to avoid the worst of the inflationary problems,” Guckes said. “Increased environmental and labor regulations could slow the pace of new construction while driving up costs.”

In either scenario, Guckes suggested the industry will soon have clarity to resume or revise plans based on the final outcome after Election Day.